Never Miss a Beat: Get a snapshot of the issues affecting the IT industry straight to your inbox.

Financial Planning, Budgeting and Forecasting in Uncertain Times

Fast-changing business conditions call for agile planning, budgeting and forecasting. Learn why best-in-class companies are better at forecasting, collaborating, reducing budget cycle times and analyzing and reporting on planning, budgeting and forecast data.

11 Min Read

Planning, budgeting, and forecasting lay the foundation for any effective business plan. Economic uncertainty makes it difficult to set clear goals and objectives and sustain a financial plan which supports them. Organizations must become more agile with their planning, budgeting and forecasting capabilities -- now more critical than ever for success and survival during volatile economic times. The business climate is characterized by change and compounded by global influences spawning unforeseen stresses and squeezed margins.

In a 2008 Financial Planning and Budgeting survey of more than 150 companies, Aberdeen Group found subtle shifts in pressures impacting the planning, budgeting and forecasting process. While speed, agility and accuracy dominated the horizon last year, Aberdeen expects the need to improve agility to adapt to changing conditions to be the number-one pressure facing companies in 2009. This article presents an executive summary of a January 2009 update entitled Financial Planning, Budgeting and Forecasting: Managing in Uncertain Times. Read on to learn what best-in-class companies are doing to plan, budget and forecasting with improved agility and accuracy.

Defining Terms

Aberdeen defines financial planning as the process by which a business documents and communicates its strategic objectives in financial terms. A financial planning exercise typically contains detailed plans and budgets, as well as analysis capabilities to show how the objectives are to be realized. Budgeting is (typically) an annual process that often starts with the prior year’s actual performance data, and includes the creation of detailed financial budgets showing expected future performance at a top-line and detailed level across the entire organization. Forecasting is a process by which businesses adjust future expectations based on recent actual performance resulting in the production of an updated forecast document. This can (but does not typically) include adjustments to the budget. Forecasting, re-forecasting, or “rolling-forecasting” can occur multiple times during a budget period, and can span time from one fiscal period to the next.

Companies are now feeling even more pressure to respond to the turbulent economy with increased agility. Not only have general markets become more volatile, the economy has plunged deeper into a recession, causing the reevaluation of many plans and budgets, shifting focus to a different set of objectives, making the more dynamic forecast a much more critical component of the process.

Best-in-Class Strategies

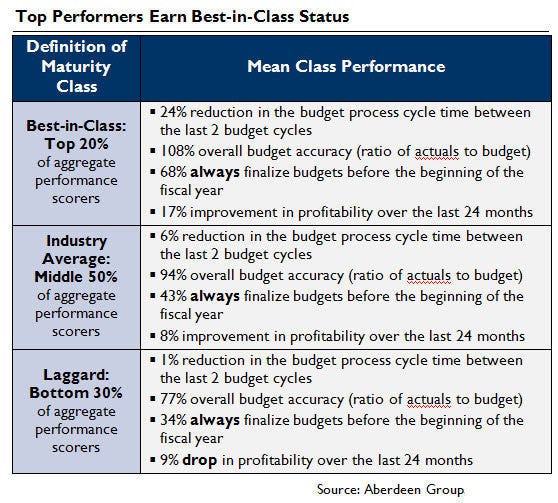

Aberdeen used four key performance criteria to distinguish the Best-in-Class from Industry Average and Laggard organizations (see table below). We first evaluated the budget process itself, including year-over-year improvements in the cycle time, which influences the organization's ability to finalize budgets prior to the beginning of the new fiscal period. We then looked at the accuracy of the overall budget and also tempered this with the ability to grow profits over the last 24 months. Without preservation or improvements in profitability, the overall goals of the planning and budgeting process are compromised.

In determining Best-in-Class performance in terms of budgeting, Aberdeen viewed 100% accuracy as the ideal. Yet realistically, companies will (and should) execute plans to maximize revenue and profits and therefore must take into account changing business conditions, perhaps sacrificing budget accuracy for the overall health of the business. Therefore Aberdeen penalized companies more for over-spending and under-performing in terms of revenue than for under-spending and exceeding revenue targets.

Strategic Actions

(click image for larger view)

The shift in Best-in-Class strategic actions from 2008 to 2009 is far from subtle. We see a complete flip in terms of priorities year over year. The top strategy from 2008, automating process flows, is now at the bottom of the list while last year's last place finish, improving data quality, is this year's main priority. Why the shift? First, 100% of the Best-in-Class have invested in applications to assist in the planning process, which inherently brings process automation into play. Now they must turn their attention to making better use of these applications through the formalization and development of processes built around these applications. The most important element of that process refinement is now insuring the quality of the data presented by these applications. With the proliferation of data today, decision makers have become increasingly dependent on it. Yet as the volume increases, we run the risk of the quality diminishing (click on the "Strategic Actions" Chart above).

By eliminating manual steps and automating the data gathering process itself, results are significantly enhanced. This also creates the opportunity to involve more decision-makers from various areas of the business, whether defined by job role or level within the organization. Requirements for Success

The selection of a financial planning, budgeting and forecasting solution (which may involve separate components or can be obtained as a packaged solution) and the integration of these capabilities with business intelligence and business process management systems plays a crucial role in the ability to drive profits.

Aberdeen Group analyzed the aggregated metrics of surveyed companies to determine whether their performance ranked as Best-in-Class, Industry Average, or Laggard. In addition to having common performance levels, each class also shared characteristics in five key categories: process (the approaches they take to execute their daily operations); organization (corporate focus and collaboration among stakeholders); knowledge management (contextualizing data and exposing it to key stakeholders); technology (the selection of appropriate tools and effective deployment of those tools); and performance management (the ability of the organization to measure their results to improve their business). These characteristics serve as a guideline for best practices, and correlate directly with Best-in-Class performance across the key metrics.

Based on the findings of our research and interviews with end users, Aberdeen's analysis of Best-in-Class respondents demonstrates that a combination of process, organizational, knowledge and performance management capabilities combined with specific technology enablement is likely to lead to top performance. The following sections detail these findings.

Forecasting Capabilities

(click image for larger view)

Process. End user organizations have clearly identified that the top business pressure driving their planning, budgeting and forecasting initiatives is the need to become more agile, particularly during the current economic uncertainty. This highlights the top-most Best-in-Class process capability -- the ability to re-forecast the business as conditions change. For some companies, this may be a bi-annual or quarterly process. In extreme cases, it may require the ability to re-forecast on an ad hoc basis without a formal closing of books at month-end or quarter-end. Best-in-Class companies are 36% more likely to have developed this capability, either through internal process improvements, technology, or both (click on the "Forecasting Capabilites" chart at right).

In addition to re-forecast capability, Best-in-Class companies are also more apt to incorporate business drivers into their ongoing forecasting process. This becomes particularly important in scenarios that involve volatile drivers (such as the the price of raw materials or the availability of talent). While a third or more of top and average performers are currently able to incorporate business drivers into the forecasting process, only a quarter of Laggard companies have obtained this ability. A combination of both process capabilities provides the most compelling on-going forecast process for use during uncertain and unstable economic scenarios.

Organization. The planning, budgeting and forecasting process cannot be successful if it is conducted in a vacuum or without the proper level of collaboration from internal stakeholders. Best-in-Class companies are more likely to prioritize collaboration from all three directions during the planning and budgeting process: top-down, bottom-up and a combined top-down-bottom-up approach.

It is not enough to establish a planning and budgeting process that only allows for collaboration in one direction. As an enterprise, Best-in-Class companies are more likely to allow a combined approach and therefore are also more likely to incorporate a formal collaboration capability whether the budgets and related documents are being reviewed from the top-down or from the bottom-up.

Knowledge Management. Successful budgeting initiatives are measured in many ways, and respondents have indicated that the cycle time from initial draft to final approved budget and forecast is important. Best-in-Class companies have reduced their cycle times by 24% in the past year-over-year period, compared to only 5% of all others. In fact Laggard companies have seen virtually no decrease at all. Interviews with respondents reveal that one of the top methods for reducing cycle time is to formalize and automate the planning, budgeting and forecasting steps and offer end users a guided step-by-step process.

Highly advanced organizations will also automate the triggers that alert planning, budgeting and forecasting stakeholders to changes and process exceptions that need to be addressed. This involves the ability to set business rules that are based on the step-by-step process as defined in the capability described previously, and the ability to tie specific process events (such as missing an approval on a budget submission) to alert actions that are sent to specific individuals with the authority to accept or reject the current document or iteration. Technology. There are several technology management aspects to achieving a Best-in-Class planning, budgeting and forecasting result. Process exceptions are one type of event that can trigger alerts, and there are also internal and external business events that can and should trigger automated alerts to stakeholders.

External events can include broad industry factors such as a rise in raw materials costs, a political or socio-economic shift in a major geographic market, or specific external forces such as a new competitor entering a market. Internal events, such as the loss or unplanned leave of key personnel, are more often integrated into the planning process by Best-in-Class companies.

Another technological edge among Best-in-Class companies involves the ability to perform in-depth analysis and reporting on planning, budgeting and forecast data. The granularity of the analysis and reporting directly impacts the depth of understanding of the data and the quality of planning and budgeting decisions that result. Multi-dimensional reporting, with the ability to perform roll-ups (at any level), helps organizations view performance from many perspectives and permutations, and instantly roll up the new perspective in order to see a consolidated result.

Once roll-ups and summaries are delivered, Best-in-Class companies are more likely to be able to drill down to successively detailed and granular levels of the data. This allows for enhanced analysis and rapid understanding of the effects of decisions made at the summary level on individual departments or line items within a budget or forecast. This is critical to the ability to improve cycle times and accuracy while quickly responding to changing conditions and understanding how changes affect the lowest levels of the organization.

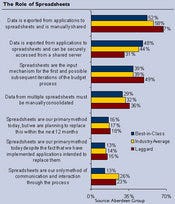

Over the past year, we have found that spreadsheets continue to be an integral part of the overall equation. Best-in-Class companies are less likely to use spreadsheets in almost every aspect of planning, budgeting and forecasting than their Industry Average and Laggard counterparts. Interestingly, 15% of all respondents report that spreadsheets remain their primary method today despite having purchased and implemented another solution or solutions intended to replace them. Another 16% report they are planning to replace their current spreadsheet-based approach within the next 12 months.

The Role Of Spreadsheets

(click image for larger view)

One of the most popular features of operational applications is the ability to export data directly to a spreadsheet application, so it is not surprising that this is the most popular role that spreadsheets play. But it is the level of control and access to this data that is critical to understand. Best-in-Class companies are far less likely to export data into manually shared spreadsheets at the initiation of a planning/budgeting/forecasting project, and are also less likely to use spreadsheets as the input mechanism for the first and possibly subsequent iterations of the overall process. Best-in-Class companies are less than half as likely to identify spreadsheets as the only communication mechanism throughout the process (click on the "Role of Spreadsheets" chart at right).

Performance Management. Finally, in addition to the performance results described in the Competitive Framework, Best-in-Class companies are achieving far greater performance when it comes to providing access and visibility to process stakeholders.

Best-in-Class companies have improved visibility (and therefore participation) by more than three times the rate of Laggard companies, and 50% greater than Industry Average companies.

Visibility is also associated with organizational buy-in, a factor that was discussed with respondents. Perhaps more than any quantifiable metric that can be measured, the degree to which an enterprise "buys in" to the planning, budgeting and forecasting process, the higher likelihood of a smoother, more accurate and ultimately more agile process overall. This visibility can be gained through technologies including reporting, dashboards, performance management applications, and other analytical and visualization tools that enable a higher degree of visibility and access to relevant information.

What's Next?

Whether a company is trying to move its performance in Financial Planning, Budgeting and Forecasting from Laggard to Industry Average, or Industry Average to Best-in-Class, Aberdeen's "Financial Planning, Budgeting and Forecasting: Managing in Uncertain Times" report offers a number of suggested "steps to success." The full report also includes more than a dozen tables and charts as well as case studies and detailed research not presented in this executive summary. The free report (registration required) can be accessed here: http://www.aberdeen.com/summary/report/benchmark/5675-RA-planning-budgeting-forecasting.asp

About the Author

You May Also Like

More Insights